Introduction: Why 65% of UK Drivers Can’t Afford a Replacement After a Write-Off

Buying a car represents one of life’s biggest financial decisions. Yet most drivers overlook a critical financial risk: depreciation.

Consider this: A brand-new car can lose 35% of its value in the first year alone and up to 70% over three years. If your vehicle is written off during this period, your comprehensive car insurance will only pay the market value at the time of the loss—not what you originally paid.

The gap between these two figures can cost you thousands of pounds.

Recent research from ALA Insurance reveals:

- 34% of UK drivers have written off a car at least once

- 65% of Brits cannot afford a replacement vehicle using only their insurance settlement

- 49% of drivers say they would struggle financially if they wrote off their car today

This is where ALA Gap Insurance becomes invaluable.

What Is ALA Gap Insurance? Understanding the Basics

GAP stands for Guaranteed Asset Protection. At its core, ALA Gap Insurance bridges the financial shortfall between what your car insurance company pays and the amount you originally paid for the vehicle.

How It Works in Real Terms

Imagine you purchase a new BMW for £48,299. One year later, a flood damages your vehicle beyond repair, and your comprehensive car insurance settles the claim at just £33,299 (reflecting market depreciation).

The gap: £15,000

Without gap insurance, you’d face this loss personally. With ALA’s Back to Invoice Plus policy, they cover this entire £15,000 shortfall—allowing you to afford a replacement vehicle without out-of-pocket expense.

Who Is ALA?

ALA Insurance is a UK-based specialist provider regulated by the Financial Conduct Authority (FCA). Unlike dealership gap insurance sold at the point of purchase, ALA:

- Operates independently

- Does not work on commission

- Provides clearer policy terms

- Offers longer coverage periods (typically up to 5 years)

- Delivers more competitive pricing

Industry Recognition:

- 4.9-star rating on Trustpilot (18,000+ reviews)

- 5-star Defaqto rating (highest insurance quality rating available)

- Best Customer Service in Financial Services – UKCXAs 2024

- Finalist – Institute of Customer Service Awards

ALA Gap Insurance: Complete Policy Types Explained

ALA offers five distinct policy types tailored to different ownership situations. Choosing the right one is essential—each protects against different financial risks.

1. Back to Invoice Plus (RTI) GAP Insurance

Best for: New and nearly-new vehicles (up to 10 years old)

This is the most popular policy type. It covers the difference between:

- Your insurance company’s payout, OR

- The original invoice price you paid

Whichever is higher at the time of claim

Eligible vehicles: Purchased within the last 180 days (or 365 days if you have new-for-old cover)

Why it matters: Early depreciation is most severe in the first few years, making this ideal for PCP/HP financed vehicles.

Real example: Ahmed bought a Kia Sportage for £32,000. Two years later, a accident resulted in a total loss. Insurance settlement: £22,500. With Back to Invoice Plus, ALA pays out £9,500 to cover the gap.

2. Vehicle Replacement Plus GAP Insurance

Best for: Vehicles subject to rapid market price increases

This policy covers the gap between your insurance settlement and the cost of a brand-new equivalent replacement model—protecting against market inflation.

Coverage includes: New car replacement (similar make, model, and age to your original purchase)

Eligible vehicles: New and used vehicles up to 7 years old, with fewer than 80,000 miles, delivered within 90 days of policy start

Why it matters: During periods of supply chain disruption or market volatility, replacement vehicles may cost significantly more than when you bought yours.

3. Contract Hire Plus GAP Insurance (Lease)

Best for: Leased vehicles and contract hire agreements

Covers shortfalls related to:

- Outstanding lease/rental payments owed to the finance company

- The gap between insurance payout and vehicle value

- Includes up to £3,000 of your initial rental deposit cover

Eligible vehicles: New and used vehicles on contract hire, delivered within the last 365 days

Why it matters: Leasing creates unique financial exposure—you owe money on a vehicle you don’t own outright.

4. Agreed Value GAP Insurance

Best for: Older vehicles or specialist cars (no age/mileage restrictions)

Rather than calculating depreciation based on market value, this policy uses an agreed value established at the time of purchase.

Coverage: Pays the difference between current market value settlement and the retail value at purchase time

Eligible vehicles: Vehicles listed on Glass’s Guide (classic cars, specialist models, older vehicles)

Why it matters: Older cars have less predictable values; this removes uncertainty.

5. Hire & Reward GAP Insurance (Commercial Vehicles)

Best for: Taxis, private hire, and commercial delivery vehicles

Covers the shortfall between purchase price and insurance settlement for commercial use vehicles.

Policy limits: Up to £50,000 vehicle value

Additional benefits:

- Includes contribution towards car hire while claim is processed

- Generous excess cover included

- Underwritten by highly-rated Hiscox

Real Claim Example: How ALA Gap Insurance Pays Out

Joe’s BMW Story (Actual Case Study)

Joe purchased a BMW 3-Series for £48,299 new in 2023.

What happened: In 2025, the vehicle was declared a total loss due to severe flood damage following heavy rainfall.

Insurance settlement: £33,299 (market value depreciation)

The shortfall: £15,000

ALA’s payout: £15,000 via Back to Invoice Plus policy

Outcome: Joe received full coverage of the gap, allowing him to replace his vehicle without additional financial burden.

How Much Does ALA Gap Insurance Cost in 2026?

Gap insurance premiums vary based on:

- Vehicle value

- Financing method and remaining balance

- Policy type selected

- Coverage duration

Typical Costs

- Budget policies: £100–£200 for multi-year coverage

- Standard coverage: £150–£300 annually

- Premium coverage: Up to £400+ (for high-value vehicles or longer terms)

Transparent pricing: ALA’s online quoter provides exact breakdown before purchase—no hidden fees.

Cost compared to other providers:

- Dealership gap insurance: Often £500–£1,000 (heavily commission-based)

- ALA independent pricing: 50–70% cheaper than dealership alternatives

ALA Gap Insurance vs. Dealership GAP Policies: Key Differences

| Factor | ALA Independent | Dealership GAP |

| Pricing | Transparent, competitive | High, commission-driven |

| Sales Pressure | None—UK-based team on salary | Significant—sales commission |

| Policy Duration | Up to 5 years | Often 1–3 years only |

| Flexibility | High—multiple policy types | Limited options |

| Documentation | Clear, provided upfront | Often rushed at point of sale |

| Claim process | Streamlined, 99% payout rate | Variable—often delayed |

| Excess cover included | Yes (£250–£500 as standard) | Rarely included |

The verdict: Independent ALA policies offer significantly better value than dealership alternatives.

What Does ALA Gap Insurance Cover? Comprehensive Breakdown

ALA Gap Insurance COVERS:

✅ Total loss following an accident – Vehicle declared a write-off by insurer

✅ Vehicle theft (unrecovered) – When stolen car is never recovered

✅ Fire damage – Vehicle damaged beyond repair by fire

✅ Flood damage – Write-off due to flooding or water damage

✅ Outstanding finance shortfall – Covers gap between payout and remaining loan balance

✅ Negative equity (during policy term) – Covers where vehicle value drops below outstanding finance

✅ Claims made within 120 days – Extended window to submit claim documentation

✅ Car insurance excess – £250–£500 included as standard cover

ALA Gap Insurance DOES NOT COVER:

❌ Mechanical failures – Engine, transmission, electrical problems

❌ Routine wear and tear – Normal depreciation without total loss

❌ Minor accident repairs – Bumper damage, scratches, small dents

❌ Vehicles without comprehensive insurance – Gap insurance requires valid comprehensive cover

❌ Negative equity transferred from previous finance – Only covers current-term negative equity

❌ Unauthorized vehicle modifications – Non-factory alterations

❌ Illegal activity-related claims – Theft during crime, unlawful use

❌ New-for-old cover already active – Cannot claim if comprehensive insurance provides replacement

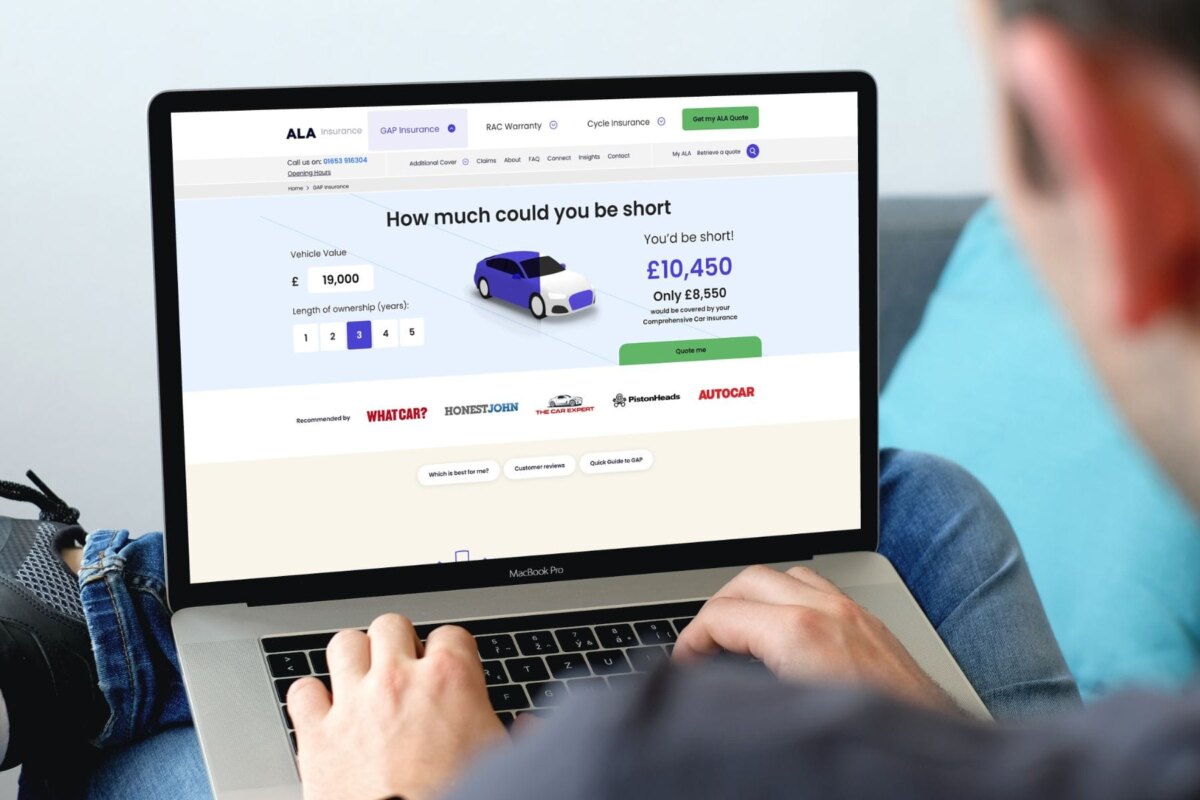

ALA Gap Insurance Calculator: See Your Real Risk

Use this interactive calculator to determine your potential financial shortfall.

Instructions:

- Enter your vehicle’s current market value (in £)

- Select your ownership duration (1–5 years)

- View your estimated depreciation and potential gap

Try the Calculator Below:

Vehicle Value: £ [Input field: 28000]

Years of Ownership:

- 1 year

- 2 years

- 3 years

- 4 years

- 5 years

Results (Example: £28,000 vehicle, 2 years ownership)

| Metric | Amount |

| Original purchase price | £28,000 |

| Market value after 2 years | £18,200 |

| Total depreciation | £9,800 (35%) |

| Insurance would pay | £18,200 |

| Without GAP insurance, you’d lose | £9,800 |

| ALA Gap Insurance covers | £9,800 |

Who Should Consider ALA Gap Insurance?

✅ ALA Gap Insurance is IDEAL for:

- New car buyers – Maximum depreciation risk in first 3 years

- PCP finance users – Monthly payments continue until finance ends

- HP finance users – Outstanding balance can exceed vehicle value

- Lease/contract hire drivers – Complex financial obligations

- High-value vehicle owners – Greater absolute loss amount

- First-time financed car buyers – Less experience managing financial risk

- Vehicles kept 3+ years – Extended exposure to depreciation

❌ ALA Gap Insurance may be LESS NECESSARY for:

- Vehicles purchased outright (at low price)

- Older vehicles (minimal remaining depreciation)

- Short ownership periods (minimal risk exposure)

- Drivers with substantial savings buffer (can absorb loss)

- Used vehicles with high mileage (limited depreciation remaining)

ALA Gap Insurance vs. Standard Comprehensive Car Insurance

Common misconception: “My comprehensive insurance covers everything.”

Reality: Comprehensive insurance only pays the vehicle’s current market value at the time of loss—not the original purchase price.

The Gap Explained:

| Scenario | Without GAP Insurance | With ALA GAP |

| Vehicle purchased for | £30,000 | £30,000 |

| After 2 years, market value | £20,000 | £20,000 |

| Total loss occurs | Total loss | Total loss |

| Comprehensive insurance pays | £20,000 | £20,000 |

| Your out-of-pocket loss | £10,000 | £0 |

| Your actual cash position | Must pay £10k to replace | Fully covered for replacement |

The Claims Process: Step-by-Step

Step 1: Report to Your Comprehensive Insurer

Contact your primary car insurance provider immediately after the loss (accident, theft, fire, flood).

Step 2: Your Insurer Issues Settlement

Your comprehensive insurer assesses the vehicle and issues a settlement figure at current market value.

Timeline: Typically 5–15 days

Step 3: Gather Documentation

Collect:

- Claim reference number from your insurer

- Settlement letter (showing payout amount)

- Original vehicle invoice/purchase receipt

- Policy documents

- Photos of damage (if available)

Step 4: Submit to ALA

Send documentation to ALA via their online portal or post.

Timeline: ALA reviews within 5–7 working days

Step 5: ALA Calculates Gap Amount

ALA determines the eligible gap based on policy terms.

Calculation example:

- Original invoice price: £28,000

- Insurer settlement: £19,500

- Eligible gap: £8,500

Step 6: ALA Pays Out

Payment made to:

- You directly (if vehicle owned outright), OR

- Your finance company (if outstanding loan exists)

Timeline: Typically 7–14 days from approval

Frequently Asked Questions: ALA Gap Insurance

General Questions

Q: What exactly does GAP stand for? A: Guaranteed Asset Protection. It’s a specialized insurance that guarantees protection against financial loss from vehicle depreciation.

Q: Is GAP insurance compulsory? A: No. It’s optional insurance that complements your comprehensive coverage. However, if you’re financing a vehicle, your lender may recommend it.

Q: Can I get GAP insurance after I’ve bought the car? A: Yes. You can purchase most ALA policies within 180 days of purchase (up to 365 days for new-car replacement cover).

Q: Does every vehicle need GAP insurance? A: No. Low-value vehicles or outright purchases with minimal depreciation remaining may not need it. Use our calculator to assess your personal risk.

Coverage Questions

Q: Will GAP insurance cover negative equity? A: Yes—but only negative equity that exists during the policy term. Negative equity transferred from a previous finance agreement is excluded.

Q: If my car’s written off but I have new-for-old insurance coverage, does ALA still pay? A: No. If your comprehensive policy provides new-car replacement cover, ALA cannot pay a gap claim. However, ALA can provide extended eligibility (up to 365 days) for certain policy types.

Q: Can I claim multiple times on my GAP insurance policy? A: Generally, no. Most GAP policies cover one total loss event. After a claim, you’d need to purchase a new policy for future protection.

Q: Does GAP insurance cover my personal belongings in the car? A: No. GAP insurance only covers the vehicle’s financial value gap—not personal items, driving equipment, or accessories.

Cost & Pricing Questions

Q: Why is ALA cheaper than dealership GAP insurance? A: Dealership gap insurance includes significant commission costs (often 40–60% of the premium). ALA operates independently with no commission-based salesforce, passing savings directly to customers.

Q: Can I pay for GAP insurance in monthly installments? A: Yes. ALA offers flexible payment options including monthly installments via the quote system.

Q: Is there an age/mileage limit for vehicles? A: Depends on policy type:

- Back to Invoice Plus: Up to 10 years old

- Vehicle Replacement Plus: Up to 7 years old, under 80,000 miles

- Agreed Value: No age/mileage limit (if listed on Glass’s Guide)

Claims & Payout Questions

Q: How long does it take for ALA to pay out a claim? A: Typically 7–14 days from claim approval. ALA processes claims quickly once documentation is verified.

Q: What’s ALA’s claim payout rate? A: 99% (if your comprehensive insurance approves a total loss, ALA pays).

Q: What happens if I don’t have comprehensive insurance when I make a claim? A: ALA cannot pay. Gap insurance requires valid comprehensive coverage to exist.

Q: Can I make a claim more than 120 days after the incident? A: No. ALA requires claims to be submitted within 120 days of the loss event.

Policy & Regulation Questions

Q: Is ALA regulated? A: Yes, completely. ALA is FCA-authorised (Financial Conduct Authority), ensuring:

- Fair sales practices

- Clear policy information

- Consumer dispute resolution

- Complaint handling procedures

Q: What if I need to make a complaint? A: ALA has a formal complaints procedure with escalation to the Financial Ombudsman Service if needed.

Q: Can I transfer my GAP insurance if I sell the car? A: Typically no. GAP insurance is tied to the original vehicle and ownership situation. You’d need a new policy for a different vehicle.

Why ALA Gap Insurance Stands Out in 2026

Award-Winning Service

- Best Customer Service in Financial Services (UKCXAs 2024)

- 4.9-star Trustpilot rating from 18,000+ real customers

- 5-star Defaqto rating (top financial service quality rating)

Financial Protection

- 99% claims payout rate – Industry-leading

- £250–£500 excess cover included – No additional cost

- No admin fees – Full transparency

- Underwritten by A-rated insurers – Financial & Legal, Hiscox

Customer-Centric Approach

- No commission-based sales – Salaried staff provides honest advice

- 120-day claim window – Extended time to submit documentation

- Independent pricing – 50–70% cheaper than dealership alternatives

- Clear policy documents – No hidden exclusions or surprise terms

Market Recognition

- Recommended by: What Car?, Auto Trader, Honest John, The Car Expert

- Best Price Guarantee – Matches competitor quotes

- Multiple policy types – Cover for every vehicle and situation

Step-by-Step: Getting an ALA Gap Insurance Quote

Option 1: Online (2-3 Minutes)

- Visit ala.co.uk/gap-insurance

- Click “Get a Quote” button

- Enter vehicle details:

- Vehicle registration/VIN

- Purchase price

- Purchase date

- Financing method (PCP, HP, cash, lease)

- Select policy type (Back to Invoice Plus is most common)

- Receive instant quote breakdown

Option 2: Phone Support (5 Minutes)

Call 01653 916304 (9:30 AM – 5:00 PM weekdays)

Speak with a UK-based advisor who can:

- Explain policy differences

- Calculate exact quotes

- Answer specific questions

- Process purchase immediately

Option 3: Callback Request

Use ALA’s website contact form to request a callback within 24 hours.

Final Verdict: Is ALA Gap Insurance Worth It in 2026?

The Financial Reality

With new car prices at record highs and depreciation accelerating in early ownership years, ALA Gap Insurance has become a practical necessity—not an optional luxury.

The math is simple:

A £30,000 vehicle loses £10,500 in value within 2 years. If that vehicle is written off during this high-risk period:

- Without GAP insurance: You lose £10,500

- With ALA GAP insurance: You lose £0

- ALA premium cost: £150–£250

Return on investment: Breakeven within a single claim.

Who Should Buy

✅ Definitely: New car buyers, PCP/HP users, high-value vehicles, owners keeping cars 3+ years

⚠️ Consider: Finance agreements, tight financial situations, multi-car household with shared risk

❌ Probably not: Low-value outright purchases, minimal remaining depreciation, strong financial reserves

Why ALA Specifically

Among gap insurance providers, ALA delivers:

- Transparent pricing – No dealership markup

- Industry recognition – Award-winning service proven by 18,000+ reviews

- Better terms – Longer coverage, included excess cover, no admin fees

- Reliable payouts – 99% claims approval rate

- Regulatory protection – FCA-authorised, complaint-resolution available

Take Action Today

Don’t leave your vehicle’s financial protection to chance.

Get your free ALA Gap Insurance quote now:

- Online: ala.co.uk/gap-insurance (2 minutes)

- Phone: 01653 916304 (UK team, no commission)

- Callback: Request via website contact form

Or use our calculator above to see your exact financial risk.

Every day you drive an unprotected vehicle is another day at risk of a £5,000, £10,000, or £15,000+ financial loss.

ALA Gap Insurance costs just pence per day—but protects you from thousands.

Additional Resources

- What Car? Recommendation – Trusted by millions of UK car buyers

- Honest John Reviews – Independent consumer feedback

- Defaqto 5-star rating – Financial service quality guarantee

- Trustpilot Reviews – 4.9 stars from 18,000+ customers

- Institute of Customer Service Awards – Finalist for customer excellence

You may also read: