UK Mortgage Rates Comparison Overview

A UK mortgage rates comparison is one of the most important steps for anyone looking to buy a home, remortgage, or invest in property in 2026. Mortgage rates directly impact how much you will pay every month and the total cost of your loan over time. Even a small difference in interest rates can lead to significant savings or extra costs over the lifetime of a mortgage. This is why borrowers are increasingly focusing on comparing lenders instead of choosing the first available offer from a bank.

In today’s market, mortgage rates in the UK are influenced by economic conditions, inflation trends, and the Bank of England’s base rate decisions. However, lenders also apply their own internal risk assessments, meaning two borrowers with similar profiles may still receive different offers. Because of this variation, a structured comparison is essential. Understanding how different lenders price their products helps buyers avoid expensive deals and identify more affordable mortgage options tailored to their financial situation.

How UK Mortgage Rates Work

Mortgage rates in the UK represent the interest charged by lenders when you borrow money to purchase a property. These rates are applied to the outstanding loan balance and determine both your monthly repayments and the total amount paid over the mortgage term. When conducting a UK mortgage rates comparison, it is important to understand that rates are not fixed universally and vary depending on borrower circumstances, property type, and deposit size.

Lenders calculate mortgage rates based on several key factors including credit history, income stability, loan-to-value ratio, and market conditions. A lower risk borrower typically receives better rates, while higher risk applicants may face higher interest charges. Additionally, fixed and variable rate structures influence how payments behave over time. Fixed rates remain stable for a set period, while variable rates fluctuate depending on market movements, making it essential to compare both options carefully before making a decision.

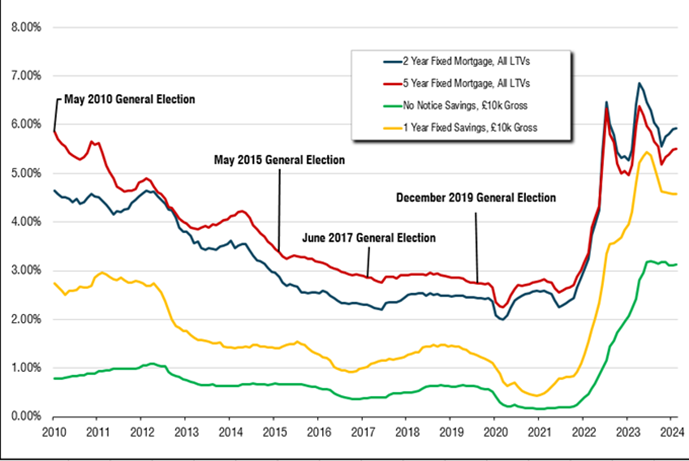

Current UK Mortgage Market Trends in 2026

The UK mortgage market in 2026 is showing signs of gradual stabilization after several years of fluctuations. Inflationary pressures have started to ease, but lenders remain cautious, meaning mortgage rates are not expected to return to the extremely low levels seen in previous years. As a result, borrowers are focusing more on affordability planning rather than chasing the lowest possible rate, which makes comparison tools more important than ever.

Another key trend is the increased demand for fixed-rate mortgages. Many homeowners prefer the stability of fixed payments, especially in uncertain economic conditions. However, some borrowers are still choosing variable or tracker products in hopes that rates may reduce in the future. This mixed approach highlights the importance of conducting a detailed UK mortgage rates comparison, as different products suit different financial strategies and risk tolerances in the current market environment.

Comparing Major UK Mortgage Lenders

When carrying out a UK mortgage rates comparison, it is important to understand how major lenders differ in their offerings. Large banks and financial institutions often provide a wide range of mortgage products designed for different borrower profiles. Some lenders focus more on first-time buyers, while others prioritize remortgage customers or buy-to-let investors. This means that the “best” lender is not universal but depends entirely on individual financial circumstances.

For example, some lenders are known for offering competitive fixed-rate deals, while others are more flexible with credit history or self-employed applicants. Mortgage brokers often highlight that lender choice can significantly impact the final rate offered. Because each institution has different lending criteria and risk models, comparing multiple options side by side is essential. A proper comparison ensures borrowers are not limited to one lender’s pricing structure and can access more suitable financial products.

Types of Mortgage Rates Explained

Understanding the different types of mortgage rates is a key part of any UK mortgage rates comparison. Fixed-rate mortgages provide stability by locking in interest rates for a specific period, typically two to five years. This option is popular among homeowners who want predictable monthly payments and protection from market fluctuations. It allows better budgeting and financial planning, especially in uncertain economic conditions where interest rates may change unexpectedly.

Variable and tracker mortgages operate differently, as they move in line with the broader market or the Bank of England base rate. These products can sometimes offer lower initial rates, but they come with the risk of future increases. Buy-to-let mortgages are another category designed specifically for property investors, often based on rental income potential. Each mortgage type serves a different purpose, and choosing the right one depends on long-term financial goals and risk appetite.

How to Find the Best Mortgage Deal in the UK

Finding the best mortgage deal requires more than simply looking for the lowest advertised interest rate. A proper UK mortgage rates comparison should also consider fees, repayment flexibility, early repayment charges, and overall affordability. Many borrowers make the mistake of focusing only on the headline rate, without understanding the full cost structure of the mortgage, which can lead to higher long-term expenses.

Using comparison tools and mortgage calculators can help estimate monthly repayments based on different rates and loan terms. Additionally, working with a mortgage broker can provide access to exclusive deals not always available directly to the public. Improving credit scores, increasing deposit size, and reducing existing debts can also improve the quality of offers received. A structured approach to comparison ensures better financial outcomes and reduces the risk of choosing an unsuitable mortgage product.

Future Outlook for UK Mortgage Rates

The future of UK mortgage rates is closely tied to inflation trends, economic growth, and central bank policy decisions. While significant rate drops are not widely expected in the short term, gradual adjustments may occur depending on market conditions. Borrowers should prepare for a scenario where rates remain relatively stable rather than dramatically decreasing, making affordability planning more important than speculation.

In this environment, staying informed becomes essential. Regularly reviewing mortgage options ensures borrowers are not locked into outdated or uncompetitive deals. A proactive approach to UK mortgage rates comparison allows homeowners to refinance or switch products when better opportunities arise. This flexibility can make a meaningful difference in long-term financial planning and help borrowers adapt to changing economic conditions more effectively.

FAQ – UK Mortgage Rates Comparison

One of the most common questions borrowers ask is how often they should compare mortgage rates. In most cases, it is recommended to review mortgage options at least six months before your current deal expires. This allows enough time to explore new offers, avoid standard variable rates, and secure a better deal. Regular comparison ensures you remain aware of market changes and do not overpay on your mortgage.

Another frequently asked question is whether fixed or variable mortgage rates are better. The answer depends on your financial situation and risk tolerance. Fixed rates provide stability and predictable payments, which is ideal for budgeting. Variable rates, however, may offer lower initial costs but come with uncertainty. A proper UK mortgage rates comparison helps evaluate both options based on current market conditions and personal financial goals.

Many borrowers also ask whether using a mortgage broker is better than going directly to a bank. In many cases, brokers can access a wider range of deals across multiple lenders, including exclusive offers not available to the public. This can result in better rates and more suitable mortgage structures. However, direct applications may still be beneficial for borrowers with simple financial profiles. Comparing both options ensures the best possible outcome for your mortgage decision.

You may also read: Top UK Real Estate Agencies – Your Complete Guide to Finding the Best Estate Agents